Achieving Better IT and Business Services Performance

The central question for any IT service operation is not "are we following the right framework?" but "are we creating value - for the business, for end users, and for the organization as a whole?" Cost modelling, financial transparency, and sound service governance are means to that end, not ends in themselves.

The Value Creation Imperative

Improving IT and business services performance requires visibility into what services cost, what they deliver, and whether that trade-off is working. IT service cost modelling provides that visibility - mapping spend to the services and outcomes it produces, enabling honest conversations about investment priorities, and surfacing where resources are misaligned with value. This matters because IT decisions made without cost transparency tend to optimize for the wrong things: inputs over outcomes, activity over impact, legacy commitments over strategic capability. Cost modelling reorients those conversations.

Connecting Costs to Value Streams

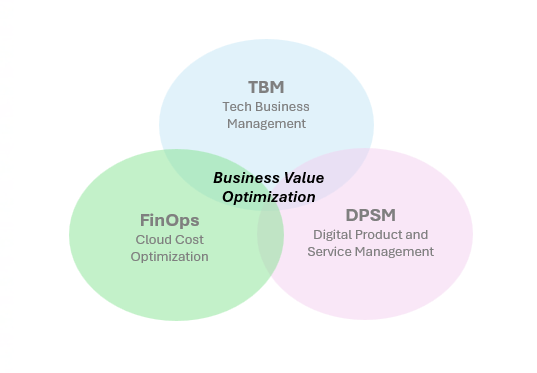

Modern operating model thinking - including the latest evolution of ITIL (now at Version 5, with its emphasis on Digital Product and Service Management and AI-enabled delivery) - frames service delivery around value streams: the actual end-to-end sequences through which IT produces outcomes for the business. Anchoring cost data to those value streams, rather than to org charts or process taxonomies, makes financial information far more useful. It shows where cost is concentrated, where demand is growing, and where investment would have the greatest leverage.

Complementary frameworks like Technology Business Management (TBM) and FinOps (for cloud environments) provide practical taxonomies for this kind of cost mapping and are widely used alongside ITIL in enterprise settings.

What Good Cost Transparency Enables

When cost data is reliable and well-structured, the benefits compound. Expenses can be allocated to the services and consumers that actually generate them, replacing arbitrary overhead pools with accountable unit economics. Internally delivered services become comparable to external alternatives on an honest, like-for-like basis. Service owners and leadership gain the ability to weigh cost against service level and make rational trade-off decisions, rather than simply defending budgets in the abstract. And when the business understands what services genuinely cost, consumption behavior changes, making demand management a natural outcome of transparency rather than a separate discipline.

A well-maintained cost model creates the conditions for better decisions at every level: which services to invest in, which to rationalize, where automation delivers genuine return, and how to demonstrate IT's contribution to enterprise value.

Here are some options for getting started:

- Define a service taxonomy using consistent language across IT, finance, and the business.

- Map value streams for your most material services to understand where costs actually accumulate end-to-end.

- Establish financial management roles and governance - a cost model owner, engaged service owners, and a leadership review cadence.

- Build the cost model around services and products, not organizational units. Map people, infrastructure, licensed platforms, third-party contracts, and (increasingly) AI workload costs to the services they support.

- Validate the model with service owners and leadership before publishing - buy-in is a prerequisite for the model to influence decisions.

- Integrate with existing management practices: service portfolio and catalog management, service level management, capacity and demand management, and configuration management all depend on and feed cost data.

- Treat the model as a living artifact - review at least annually or as the service portfolio or delivery model materially changes.

Member discussion